Revision of the Baidoa Agreement and establishing the petroleum revenue management law

Ahmed Idan Adan

May 2026

________________________________________________________________________________________

1

Oil and gas investment necessitates a comprehensive legal and regulatory framework due to the sector’s high

capital intensity and long-term nature. At the national level, such a framework typically comprises policies,

laws, and regulations that govern the industry. In addition, contractual agreements between host

governments and investing companies play a critical role. These contracts are often area-specific, outlining

the rights and obligations of the parties involved, and commonly include provisions related to operational,

financial, social, environmental, and production responsibilities.

Sectoral legislation, commonly referred to as petroleum law, act, or code, serves as the primary source of

regulatory authority. It generally addresses the roles and responsibilities of relevant governmental

institutions, licensing procedures, and the regulation of petroleum activities. Furthermore, it establishes

fiscal terms and includes provisions related to health, safety, and environmental standards, labor

requirements, local content, data management, and public accountability.

Supplementing this legislative framework is the petroleum revenue management law, which is equally

important. This law governs the collection, allocation, and management of petroleum revenues. Its primary

objective is to ensure that such revenues are managed in a responsible, transparent, and sustainable manner

for the benefit of present and future generations.

Petroleum revenue refers to the total income received by a government from the exploration, development,

and commercialization of crude oil and natural gas. This includes revenues derived from royalties, taxes,

signature bonuses, fees, government profit shares, and state participation in petroleum operations.

Petroleum revenue has unique characteristics. It is inherently finite and subject to significant volatility due

to fluctuations in global prices and production levels, making it an unreliable revenue source over the long

term. The sector also generates large economic rents that are geographically specific, which may contribute

to disputes and governance challenges. Given these characteristics, petroleum revenues require specialized

management and distribution mechanisms that differ from other types of government revenue.

Revision of the Baidoa Agreement

Despite recent progress in the development of the oil and gas sector, including the establishment of much of

the necessary legal framework, Somalia has yet to enact a comprehensive petroleum revenue management

law. Currently, the primary instrument governing petroleum revenue is the Agreement on Ownership,

Administration and Sharing of Revenues from Natural Resources (Petroleum and Minerals), commonly

referred to as the Baidoa Agreement.

This agreement, concluded in 2018 in Baidoa, represents a political framework negotiated between the

Federal Government of Somalia (FGS) and the Federal Member States (FMS). It was developed by a Technical

Committee for Facilitation and Negotiation on Federal Affairs with the objective of establishing principles for

revenue sharing from petroleum and mineral resources. The agreement has played a significant role in

2

reducing political tensions and currently serves as the principal reference point for revenue-sharing

arrangements in Somalia.

However, the Baidoa Agreement remains an incomplete framework. It lacks the necessary legal back-up,

detailed fiscal provisions, and institutional mechanisms required for effective implementation. Given that

approximately eight years have elapsed since its adoption, and considering the progress made in sector

development, there is a need to revise the agreement and integrate it into a comprehensive and legally

binding petroleum revenue management law.

Unlike the Baidoa Agreement, which was deliberated and negotiated by a limited group of political actors,

some of whom may not have possessed sufficient familiarity with the characteristics of the petroleum sector,

a formal legislative framework, such as a petroleum revenue management law, should be drafted by the

relevant competent institutions. Such legislation should also be subject to broader public participation

through structured and transparent public consultation processes before its submission to Parliament for

consideration and approval. Meaningful public engagement would not only provide valuable practical input

to the legislative process but would also strengthen the legitimacy, transparency, accountability, and

inclusiveness of the governance framework for natural resource revenues.

As the sector continues to advance and initial revenues begin to materialize for some of the licenses, the

The establishment and transparent implementation of a comprehensive revenue management law is critical.

Such a framework is essential to ensure the effective, equitable, and sustainable utilization of petroleum

resources, while mitigating the risks associated with the resource curse.

As illustrated in the table above, the listed petroleum fiscal revenues are distributed among the Federal

Government of Somalia, the petroleum-producing regional state, and the producing district within that regional state

Baidoa Agreement’s list of sub-national revenue sharing components list

3

state, and the non-producing regions. The first two revenue categories relate to profit oil sharing from

offshore and onshore petroleum operations. It should be noted that these allocations do not represent the

total government takes from production-based revenues, which ordinarily comprise royalty, profit oil share

plus corporate income tax.

The table indicates that corporate income tax, at a rate of 30 percent, is allocated exclusively to the Federal government

Government. From a fiscal administration perspective, the sub-national allocation of production-based

revenues, namely royalty, profit oil share, and corporate income tax could be consolidated into a single

revenue category for both offshore and onshore operations, rather than being presented as separate line

items.

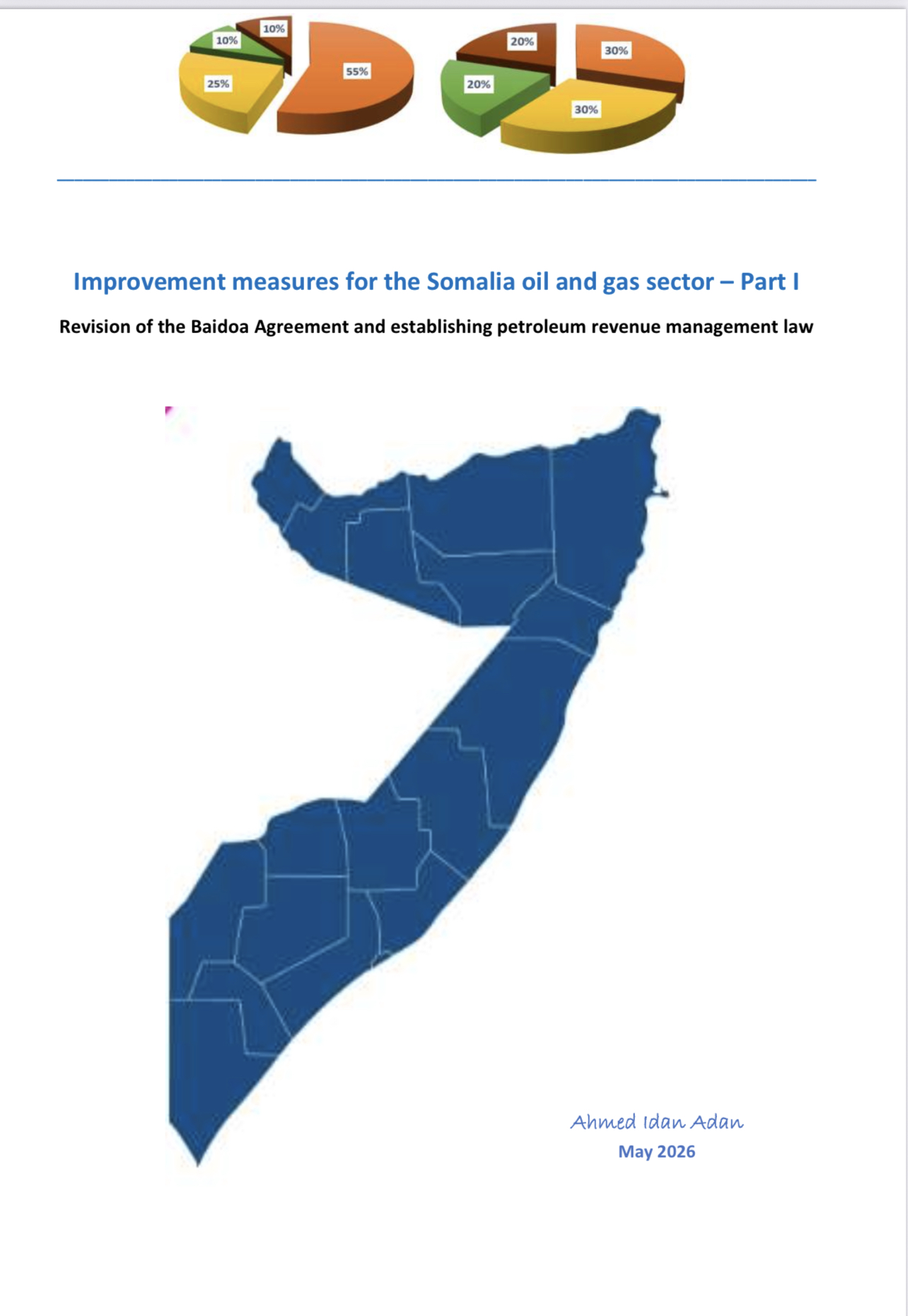

Furthermore, the allocation of offshore profit oil appears disproportionately tilted against the non-producing

regions. Under the current framework, the Federal Government receives 55 percent of offshore profit oil

share, while non-producing regions are allocated only 10 percent. Such an arrangement may not adequately

support the national cohesion and equitable resource-sharing principles that are essential to Somali unity

and state-building process. This is particularly notable given that the governing agreements explicitly

emphasize that resource-sharing arrangements should promote national unity (Article 3 of the Baidoa

Agreements). This imbalance could be addressed through several alternatives, including a reduction in the

Federal Government’s allocation, an increase in the share allocated to non-producing regions, or a

restructuring of the allocation framework whereby the non-producing regions’ share is integrated into the

Federal Government’s portion for subsequent internal redistribution.

Similarly, the onshore profit oil allocation appears heavily skewed in favor of the producing regional state

and its districts. The producing regional state is allocated 50 percent of the national profit oil share. A more

balanced allocation would be in the range of 30 to 35 percent.

Profit oil sub-nations distribution offshore and onshore

Sub-national profit oil sharing – offshore Sub-national profit oil sharing – onshore

4

In addition, the list of revenue categories does not comprehensively capture all potential government

revenues arising under the production sharing agreement framework. For example, the current Somali

production sharing agreement model provides for a withholding tax of 5 percent on gross remittances made

by contractors to subcontractors. Given that subcontracting activities in the upstream petroleum sector may

involve projects valued in the tens of millions of dollars, such tax revenues could be significant. However, the

Baidoa Agreement does not clearly specify how such revenues are to be allocated.

Likewise, the agreement does not sufficiently address revenues arising from penalties associated with

contractors’ failure to fulfill minimum work and expenditure obligations during exploration phases, including

seismic acquisition and exploratory drilling commitments. Such payments may amount to several million

dollars, yet the absence of a clearly defined allocation mechanism creates potential legal and fiscal

uncertainty.

The Baidoa Agreement also fell short of establishing a clear mechanism to address the finite and volatile

nature of petroleum revenues. As an intergovernmental agreement rather than a comprehensive petroleum

revenue management law, the Baidoa Agreement was not structured to accommodate detailed provisions

on this matter. Consequently, the consideration of future generations is only mentioned in Article 3 of the

Baidoa Agreement, without any commitment to specific revenue allocations or any indication that such

allocations would subsequently be provided for under implementing regulations.

In conclusion, Somalia’s petroleum sector institutions should urgently establish a comprehensive petroleum

A revenue management framework to regulate the collection, management, investment, and sub-national

distribution of petroleum revenues. Such legislation should also provide for the establishment of sovereign

petroleum funds, including a stabilization fund and a future generation’s fund, together with their

governance structures, fiscal rules, investment mandates, advisory mechanisms, and committees.

Furthermore, the Baidoa Agreement requires amendment to ensure a more equitable and balanced

distribution of petroleum revenues that promotes national unity and delivers broad-based economic

benefits. The current allocation framework disproportionately favors the Federal Government and

producing regions while limiting the participation of non-producing regions. In addition, the agreement

remains incomplete, as several potential revenue streams lack clearly defined allocation formulas, creating

avoidable legal and fiscal ambiguity.

(a) One-off payments, such as bonuses, penalties, and data sales.

(b) Annual payments, such as surface rental fees, administrative fees, capacity building, and other recurring

financial obligations tied to the contract area.

(c) Activity-based and production-based revenues, including royalties, various forms of taxation, profit oil

share, government participation, and other production-linked fiscal instruments.

Written by Ahmed Idan Adan